Media International Exchange 2016.12.05

Risk in the Chinese Economy and the Challenge to Political System Reform―Preparation for secular economic stagnation after shifting to a period of stable growth and the role of Japan―

The Chinese economy is maintaining its stability due to robust consumer spending

Principal economic indicators for the third quarter will be announced on October 19. The data will purportedly show the economy continuing on a gradual downtrend, considering the recent changes in exports and investment.

Generally, the GDP (gross domestic product) growth rate is estimated to be around 6.6%; should it fall below 6.5% there will be an uproar. Nonetheless, we do not have to change how we view the current Chinese economy.

If China continues to pursue its current policies in which the government is vigorously pushing forward the reduction of overcapacity under the basic policy of a "new normal," it is just a matter of time before the growth rate falls below 6.5%, and this may happen at any time.

To ensure the smooth reduction of overcapacity, which is a priority for the Chinese government, it will be more desirable if the growth rate falls below 6.5% because that will then accelerate the shakeout of inefficient companies vulnerable to harsh competition. Therefore, this scenario should be a welcome trend for reformists.

It is assumed that overcapacity reduction - the most important measure of the current year's economic policy - will remain the same next year. If this is the case, a gradual downtrend in the growth rate is supposed to continue owing to a slowdown in investment growth.

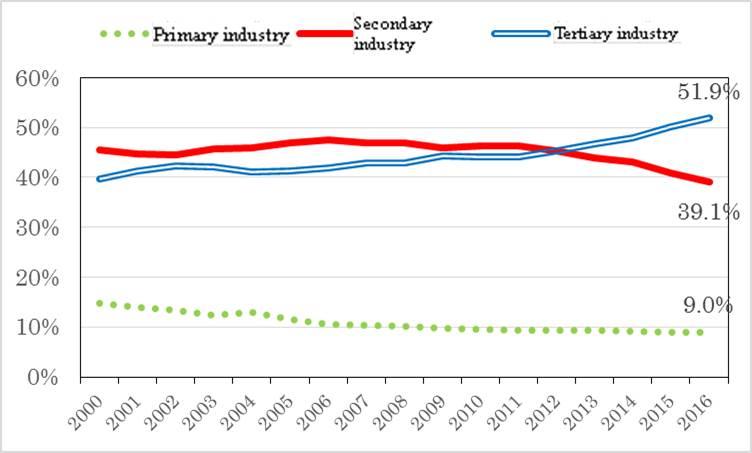

Nevertheless, it is unlikely that the growth rate will fall below 6% next year because as urbanization progresses, rapid growth in the service industry will create new employment to support income, thereby maintaining a strong consumer spending impetus (See Figure 1).

This is the mechanism which is underlying foundation of the economic growth model of the current Chinese economy. Considering the structural characteristics of progressive urbanization supported by infrastructure construction, it is difficult to imagine that this mechanism will collapse over the next few years.

Exports (calculated in dollars) have remained below the previous year's level since the second quarter of 2015. Investment in fixed assets has just made a single-digit increase over the previous year since May this year, and the growth rate has been gradually declining.

Despite that, consumer spending (the total amount of retail sales of consumer goods) has been increasing steadily in the range of 10 percent, due to the mechanism mentioned above. And the foundation of economic growth has been sustained by this robust consumption.

In recent years, the ratio of active job openings to applicants in urban areas has been gradually declining. Given this factor, the growth of wages will also be slow-moving, and therefore, consumer spending will fall below 10% before too long.

However, because the decline in income and consumer spending is more moderate compared to that of exports and investment, a significant decline is unlikely to happen even if consumer spending falls below 10%.

Price stability is another important factor to prevent recession

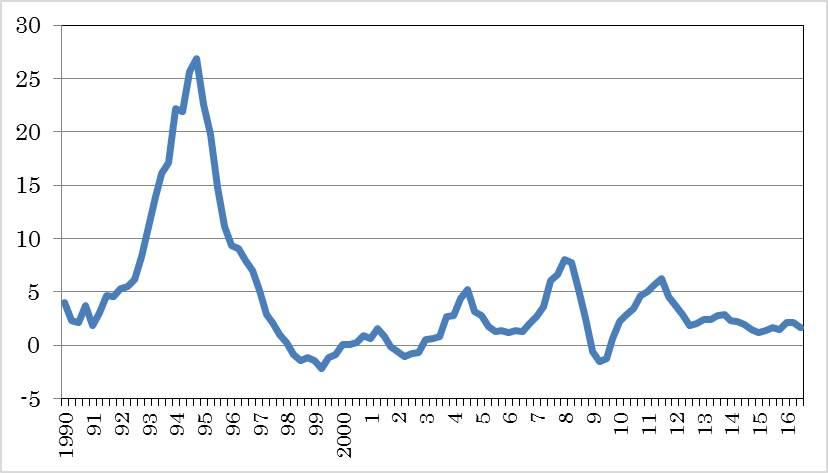

Price stability is another important factor in maintaining economic stability. China had suffered from either inflationary or deflationary trends for about 20 years, from the time it started transitioning to a market-oriented economy in the early 1990s until 2011.

However, the Xi Jinping administration has been implementing "new normal" economic policies, which aim to achieve appropriate growth rates consistent with China's economic power, and because of this, the consumer price growth rate has remained stable at around 2% for more than 4 years now (See Figure 2).

Considering that many developing countries with comparatively high economic growth rates, including India, Brazil and Indonesia, have been suffering from inflation, the current price stability in China is outstanding.

If the consumer price growth rate is high, it will be difficult to implement bold economic stimulation measures because inflation may accelerate. Conversely, if prices remain steady, bold economic stimulation measures can be implemented immediately even if there is an increased risk of falling into recession.

In this regard, China is always ready to implement bold economic stimulation measures in every respect, and this is why the risk of recession is extremely low.

The risk of an increase in non-performing loans remains low for the time being

On the other hand, the risk of an increase in non-performing loans destabilizing the economy has been widely identified. However, this, too, is more likely to be offset internally for the time being.

As the result of the vigorous government-led overcapacity reduction, many factories, mainly heavy industry, have been forced to shut down this year. Despite that fact, macroeconomic stability has been maintained.

Since the central government is trying to further accelerate the overcapacity reduction, a further decline in the growth rate is expected to continue in the second half of this year. However, a significant decline is unlikely, and the risk of a rapid increase in non-performing loans with a growth rate in the range of 6 percent will be low.

In this period, what is happening in the real estate market for Third and Fourth class cities with excessive stock of real estate properties? From a mid- to long-term perspective, demand may increase due to rapid urbanization, and so there has been only a modest decline in real estate values. For this reason, it is unlikely that non-performing loans will be a serious problem.

The decline in the growth rate of the revenues of financial institutions is also a concern.

In this respect, the central government is trying to stabilize profits through the following efforts so that the strength of financial institutions will not rapidly decline: controls on the liberalization of interest rates; securing the profit margin between deposit rates and loan rates; and preventing deterioration of profitability of lendings issued by financial institutions.

Through these efforts, even if non-performing bank loans need to be disposed of due to unrecoverable debt, this can be offset within the profit of the financial institutions for the time being.

Based on the macroeconomic behavior mentioned above, the Chinese economy will remain stable in the short run. In consideration of these circumstances, the central government is pushing forward with structural reforms swiftly and strongly while the risk of economic slowdown is still low.

If structural reforms are put off, it will be difficult to maintain macroeconomic stability into the 2020s, making reforms more difficult to carry out.

Risk of protracted recession from the late 2020s onwards

The service industry, evolving with the progress of urbanization, creates new employment and consumer spending maintains steady growth - this is the mechanism which stabilizes the current economy.

There are two major engines that sustain this stable growth: Urbanization and large-scale infrastructure construction projects, such as high speed railways and expressways. These major engines will start to lose momentum as necessary large-scale infrastructure spreads across China, the rural population decreases, and average income levels reach that of developed countries.

This is expected to happen between 2020 and 2025. Because China is a country with a population of about 1.4 billion and consists of regions with very different levels of economic development, the economic data encompassing the entire country changes very slowly.

Judging from the prospects of such structural changes, it is expected the Chinese economy will shift from a period of high growth to one of stable growth in the late 2020s.

Once China enters a stable period of growth, the progress of its economic resilience will become weaker. Recession is experienced by every developed country and it is not uncommon to require several years to recover from recession.

Protracted recession's repercussions on political instability

The government of a developed country with a democratic political system, is often accused of causing a recession, or accused of being unable to achieve economic recovery when such situations arise. The administration is then replaced by a new government through elections, which contributes to the political stability of the entire nation.

However, in a country with no established democratic political system to facilitate the smooth transfer of administration, the long-standing stagnation of the economy or inflation can often lead to public dissatisfaction and anti-government movements, resulting in political instability.

Classic examples of this include Poland at the end of the Cold War era, the Revolutions of 1989 in Central and Eastern Europe including Romania, and the "Arab Spring" that began in Tunisia, Egypt and other countries in the Arab world around 2010.

These revolutionary movements do not necessarily involve violence. However, it is indisputable that the established government as well as the class with vested interests will lose their powers or privileges, and the framework under which the nation functions will be faced with major changes.

As just described, if major changes occur in political, economic and social systems simultaneously, it is often the case that economic policy is disrupted, resulting in a protracted serious economic stagnation. Looking at a number of cases in the past, political instability does a lot of damage to people's daily lives.

If the Chinese economy falls into protracted recession under the current dictatorship of the Communist Party of China from the late 2020s onwards, the people's confidence in the Communist Party will decrease considerably.

The legitimacy of the current Communist Party of China is widely supported by the Chinese people. However, it is obvious that this support is not given for its ideology, but rather for its management capability of economic policy, which has achieved remarkable economic growth.

If the Chinese economy falls into protracted stagnation, it will prompt frustration with the policy management of the Communist Party of China, and it will then be inevitable that the people's confidence in its legitimacy will decline. If a decline in legitimacy leads to political instability, the recession will be worsened.

If China, the world's second-largest economy, falls into protracted serious recession, the world economy will inevitably be pulled into the grip of a protracted economic slump. The adverse effects this could have on Japan, a neighboring country of China, may cause immeasurable suffering.

Provision for future risks and cooperation between China and Japan

It is crucial for China to prepare for such future risks. To secure long-term stability in both its politics and its economy, China needs to establish a system which can maintain political stability in case of a protracted recession.

However, this means changes to the existing political system, which has continued since the foundation of the country, and therefore, will be an extremely difficult reform to carry out. This is not something a mediocre leader can do; even a good leader cannot achieve such reforms in a short period.

An American expert in international politics, who is familiar with China's internal affairs pointed out, "If China ever embarks on political reform, it needs to first implement experimental reforms in some parts of the country, and then gradually expand these reforms nationwide based on its experimental experiences. In order to complete reform of the whole political system in preparation for a protracted recession which is anticipated from the late 2020s onwards, China needs to start experimental reforms in some regions as soon as possible, otherwise it will be too late." I agree to this view.

However, it is vital to ensure the stability of the political foundations before taking on such a historically daunting project. If it is truly happening, a realistic scenario for the Xi Jinping administration will be to establish a staunch political foundation at the National Congress of the Communist Party of China to be convened in the fall of 2017 before embarking on this major historical project.

The Xi Jinping administration has been working on several formidably historic projects including the anti-corruption campaign, the reform of state-owned enterprises, and military reforms. Every one of these reforms is extremely challenging, and therefore, outstandingly successful results cannot be expected in the immediate future.

Nonetheless, there is no doubt the Xi Jinping administration will continue to work aggressively on these historically arduous projects.

The remaining projects are even more challenging than those that have been worked on until now. However, if nothing is done, it is inevitable that China will be hit by even more harsh realities in the future. The Xi Jinping administration is expected to respond to even more arduous challenges as a continuation of all the other projects it has dealt with so far.

Japan, a neighboring country of China, cannot interfere in China's internal affairs. However, it is possible for Japan to indirectly support economic stabilization, which will serve as a base for the bold challenges that China will tackle. More specifically, Japan can help promote Asian economic development through closer economic relations between China, South Korea and Japan, to strengthen the foundation for stable growth in East Asian economies.

Promising major cooperation initiatives include the enhancement of a win-win relationship between China and Japan through the continuous expansion of direct investment in China by Japanese companies, infrastructure construction in Asian countries, and promotion of free trade through the swift establishment of a high-level FTA (Free Trade Agreement) between China, South Korea and Japan.

It is also extremely important for Japan that China maintains its stability in politics, the economy and society from the late 2020s onwards. No one can stop the growing win-win relationship created through the increasingly closer economic relationship between China and Japan amid the tide of globalization.

With this reality in mind, it is essential for both countries to further strengthen cooperative ties in order to bolster the foundation for protracted stable growth.

(This article was translated from the Japanese transcript of Mr. Seguchi's column published by JBpress on October 19, 2016.)