Column Finance and the Social Security System 2020.08.25

【Aging, safety net and fiscal crisis in Japan】No.264: The economic growth rate assumed by the government is a pie in the sky

In this column series, Yukihiro Matsuyama, Research Director at CIGS introduces the latest information about aging, safety net and fiscal crisis in Japan with data of international comparison.

According to the GDP statistics released by the government on August 3, 2020, the GDP growth rate in the first quarter of 2020 was -0.6% in real terms and -0.5% in nominal terms compared to the fourth quarter of 2019. The GDP growth rate for FY 2019 (April 2019 to March 2020) was 0.0% in real terms and 0.8% in nominal terms. Meanwhile, at the council on economic and fiscal policy held on July 31, the government presented an outlook for the economic stagnation caused by the spread of COVID-19, as well as the medium- to long-term economic growth rate thereafter. The government set the GDP growth rate for FY2020 at -4.5% in real terms and -4.1% in nominal terms, and the rate for FY2021 at 3.4% in real terms and 3.5% in nominal terms, reflecting their expectation of a very sharp recovery. The government forecasts that the GDP growth rate from 2022 onward will gradually decline, and the real GDP growth rate in 2029, the final year of the forecast, will be at 0.8% in the baseline case and 1.8% in the growth realization case.

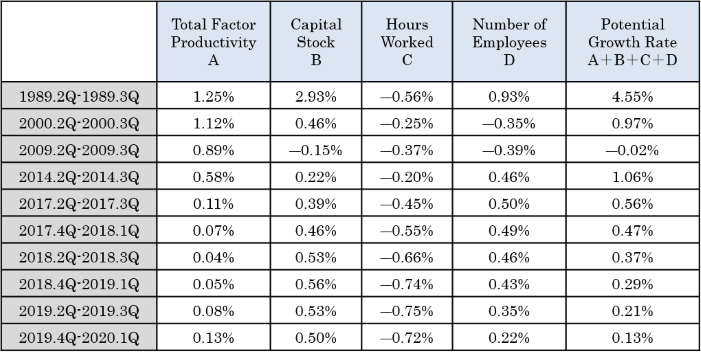

The problem with the government’s forecast is that the assumed rate of increase in the total factor productivity (TFP), which is the utilization efficiency of labor and capital, is higher than the actual results. As shown in Table 1, TFP is an important determinant of economic growth, and is assumed by the government to be at 0.7% in the baseline case. The growth realization case assumes that TFP will rise to 1.3% by 2025. However, TFP has been stagnating at around 0.1% since 2017. In 1989, at the peak of the Japanese economy, the TFP was at 1.3%. As such, judging by the current situation — in which structural reforms in the service industries (such as medical care, education, and government) have not progressed at all — the TFP cannot be expected to rise significantly.

Table 1: Factorial decomposition of potential growth rate

Source: Bank of Japan