Column Finance and the Social Security System 2018.12.11

【Aging, safety net and fiscal crisis in Japan】No.141: Total analysis of financial statements of social welfare corporations

In Column No. 17, I discussed social welfare corporations that provide welfare services on behalf of the government by operating elderly facilities, nurseries, disabled facilities, child protection facilities, hospitals, and the like. The social welfare corporation system was founded in 1951, and large subsidies have been allocated each year, but the government never summed up the financial statements of all social welfare corporations, and the market size was unknown. Therefore, the social welfare law was revised on March 2016 to create a national database of their financial statements. However, although the Ministry of Health, Labor and Welfare collected the financial statements for the 2016 fiscal year, it still has not completed the work of analysis. Then, the Canon Institute for Global Studies conducted the totalization of financial statements submitted by social welfare corporations to the Ministry of Health, Labor and Welfare.

As a result, the characteristics and issues of the financial structure of all social welfare corporations have been clarified.

(1) While the number of social welfare corporations is 20,645, about 750 of them have not submitted financial statements for the 2016 fiscal year, even after one and a half years. The Ministry of Health, Labor and Welfare has not fulfilled the responsibility of collecting them.

(2) Of the financial statements submitted, 724 are unbalance sheets in which the debits and credits of the balance sheet do not match. This suggests there is unspecified money. The Ministry has neglected the investigation of the cause. Such incomplete accounting processing has not been corrected because social welfare corporations receive tax-free preferential treatment, and there is no check by the tax office.

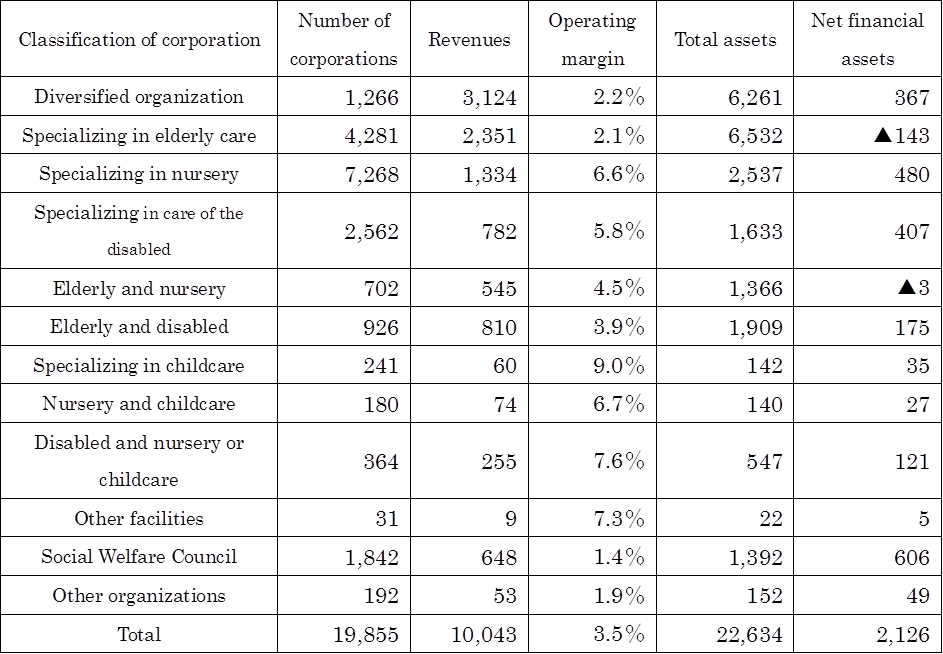

(3) As Table 1 shows, the total revenues of social welfare corporations are 10 trillion yen, the operating margin is 3.5%, the total assets are 22.6 trillion yen, and the net financial assets are 2.1 trillion yen, which is the amount obtained by deducting borrowings from financial assets.

(4) Even in the same area and the same type of facility, there are significant disparities between social welfare corporations in operating margins and net financial assets. Social welfare corporations are bipolarized into model entities that respond to the welfare needs of local residents at all times and improper organizations that run into profit accumulation.

(5) It is necessary to tax social welfare corporations to rectify financial statement deficiencies and transfer financial resources from social welfare corporations running on profit accumulation to model entities.

Table 1: FY 2016 financial data of social welfare corporations (Billion Yen)